Value At Risk Formula : Calculating Expected Shortfall CVAR in Excel. / Value at risk (also var or var) is the statistical measure of risk.. Value at risk ( var ) is the maximum potential loss expected on a portfolio over a given time period, using statistical methods to calculate a confidence level. Boudoukh, richardson, and whitelaw proposed a formula to calculate the weight for a day. It is worth distinguishing two concepts: Calculate value at risk (var) for a specific confidence interval by multiplying the standard deviation by the appropriate normal distribution factor. Value at risk (var or sometimes var) has been called the new science of risk management, but you don't need to be a scientist to use var.

What kind of variables do you need? What is value at risk ? Value at risk (var) is a statistical measurement of downside risk applied to current portfolio positions. It measures the volatility of a portfolio of assets. Value at risk (var) is a statistic used to try and quantify the level of financial risk within a firm or portfolio over a specified time frame.

How to Calculate Value-at-Risk - Step by Step from www.glynholton.com Value at risk (var) is a statistical measurement of downside risk applied to current portfolio positions. By assuming investors care about the odds of a really big. What is value at risk ? Boudoukh, richardson, and whitelaw proposed a formula to calculate the weight for a day. It measures the volatility of a portfolio of assets. The value at risk figure is widely used, so it is an accepted standard in buying, selling, or recommending assets. Value at risk (var or sometimes var) has been called the new science of risk management, but you don't need to be a scientist to use var. Value at risk is an important tool for estimating capital requirements, and is now a standard value at risk is simply the greatest expected loss over the holding period at the given confidence level.

Value at risk (var) is a measure of the risk of loss for investments.

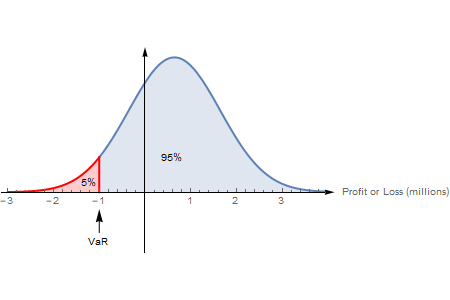

Know everything about value at risk or var here. (var is capitalized differently to distinguish it from var, which is used to denote variance.) var is widely used by financial institutions. In this video, i have explained value at risk, meaning and definition of value at risk, methods of calculation of value at risk. It estimates how much a set of investments might lose (with a given probability), given normal market conditions, in a set time period such as a day. What kind of variables do you need? Value at risk (var) is a measure of the risk of loss for investments. Value at risk (var or sometimes var) has been called the new science of risk management, but you don't need to be a scientist to use var. From a methodology point of view, the most robust results are likely to come from. You would anticipate exceeding your var amount only 5% of the time (or, 95% of the time you expect to lose less than. This article briefly compared and contrasted different methodologies which we can utilise to compute value at risk (var). Value at risk (var) is an important risk measure used by the portfolio managers across the globe. Know everything about var or value at risk here. Is it possible calculate value at risk on an asset without a time horizon?

Value at risk is an important tool for estimating capital requirements, and is now a standard value at risk is simply the greatest expected loss over the holding period at the given confidence level. Here vi is the number of variables on day i, and m is the number of days for which the. It measures the volatility of a portfolio of assets. Var is a method of calculating and controlling exposure to market risk. This article briefly compared and contrasted different methodologies which we can utilise to compute value at risk (var).

How to make a million*, and what we should do to stop you. from nms.kcl.ac.uk Value at risk (var) is a measure of the risk of loss for investments. This definition of var uses a 5% risk level: The value at risk figure is widely used, so it is an accepted standard in buying, selling, or recommending assets. Value at risk is an important tool for estimating capital requirements, and is now a standard value at risk is simply the greatest expected loss over the holding period at the given confidence level. Var can be calculated for any time period however, since uncertainty increases with time it is often. By assuming investors care about the odds of a really big. Value at risk (var or sometimes var) has been called the new science of risk management, but you don't need to be a scientist to use var. (var is capitalized differently to distinguish it from var, which is used to denote variance.) var is widely used by financial institutions.

Value at risk (also var or var) is the statistical measure of risk.

Calculate value at risk (var) for a specific confidence interval by multiplying the standard deviation by the appropriate normal distribution factor. Find details such as its concept, example, calculation, types, benefits, cons & more. In this video, i have explained value at risk, meaning and definition of value at risk, methods of calculation of value at risk. What is value at risk ? Value at risk ( var ) is the maximum potential loss expected on a portfolio over a given time period, using statistical methods to calculate a confidence level. This definition of var uses a 5% risk level: Know everything about var or value at risk here. Var can be calculated for any time period however, since uncertainty increases with time it is often. Before putting entire savings into the investments, the first thing that strikes in any investor's mind is. This article briefly compared and contrasted different methodologies which we can utilise to compute value at risk (var). Though its advantages clearly weigh more than the. Variables that are on the table are value, standard deviation, beta, market return in the above formula alpha indicates the normal deviation.sigma indicates the volatility of the underlying assets. Value at risk (var) is a statistical measurement of downside risk applied to current portfolio positions.

Value at risk (also var or var) is the statistical measure of risk. Find details such as its concept, example, calculation, types, benefits, cons & more. This definition of var uses a 5% risk level: Is it possible calculate value at risk on an asset without a time horizon? Know everything about value at risk or var here.

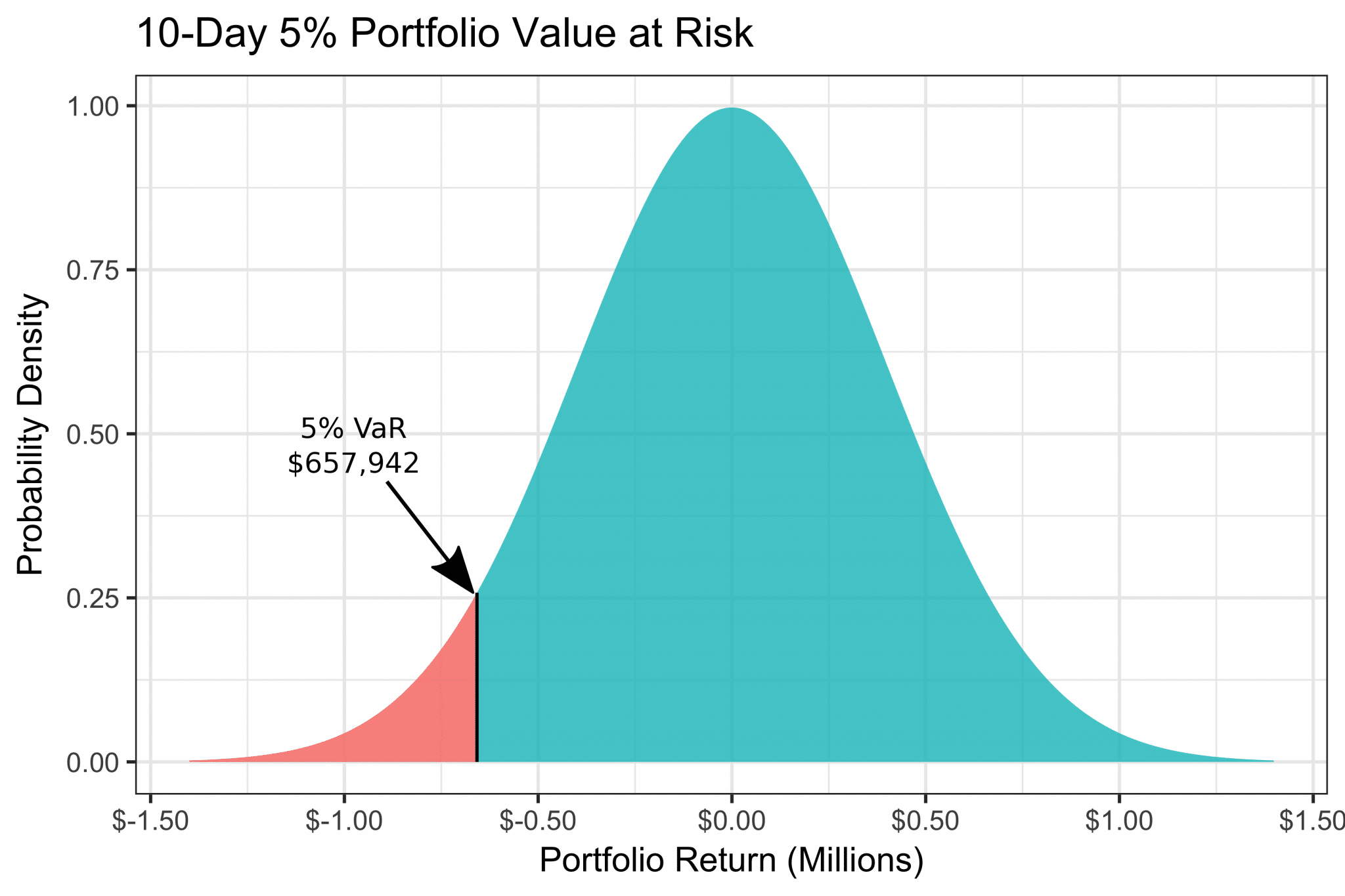

VaRImage_Annotated - cQuant.io from cquant.io This article briefly compared and contrasted different methodologies which we can utilise to compute value at risk (var). Before putting entire savings into the investments, the first thing that strikes in any investor's mind is. The weight is calculated based on the decay factor. Value at risk ( var ) is the maximum potential loss expected on a portfolio over a given time period, using statistical methods to calculate a confidence level. Value at risk (var) is a statistical measurement of downside risk applied to current portfolio positions. Var is a method of calculating and controlling exposure to market risk. Your formula for arriving at annual portfolio volatility of $7033.82 uses daily volatility of each stock. It estimates how much a set of investments might lose (with a given probability), given normal market conditions, in a set time period such as a day.

This definition of var uses a 5% risk level:

A functional relationship 1p = θ(1r) is then defined as a. You would anticipate exceeding your var amount only 5% of the time (or, 95% of the time you expect to lose less than. Though its advantages clearly weigh more than the. Boudoukh, richardson, and whitelaw proposed a formula to calculate the weight for a day. Value at risk (var) is a measure of the risk of loss for investments. It is worth distinguishing two concepts: (var is capitalized differently to distinguish it from var, which is used to denote variance.) var is widely used by financial institutions. This definition of var uses a 5% risk level: Know everything about value at risk or var here. Find details such as its concept, example, calculation, types, benefits, cons & more. From a methodology point of view, the most robust results are likely to come from. Its ease of understanding and wide acceptance by the regulatory authorities makes it even more favorable for the fund management companies to adopt. The weight is calculated based on the decay factor.

You have just read the article entitled Value At Risk Formula : Calculating Expected Shortfall CVAR in Excel. / Value at risk (also var or var) is the statistical measure of risk.. You can also bookmark this page with the URL : https://basarogg.blogspot.com/2021/05/value-at-risk-formula-calculating.html

Share Awesome

Belum ada Komentar untuk "Value At Risk Formula : Calculating Expected Shortfall CVAR in Excel. / Value at risk (also var or var) is the statistical measure of risk."

Belum ada Komentar untuk "Value At Risk Formula : Calculating Expected Shortfall CVAR in Excel. / Value at risk (also var or var) is the statistical measure of risk."

Posting Komentar